From 6 April 2017, new restrictions were imposed on the rate of tax relief available to individuals that receive rental income on residential property in the UK or elsewhere and incur finance costs (such as mortgage interest).

These restrictions mean that higher-rate taxpayers will no longer be able to offset all their mortgage interest against rental income before calculating the tax due. The changes will be phased out over a four-year period, commencing in 2017/18 tax year, and will work as follows:

• 2017/18: 75% of interest deducted as normal and 25% at basic rate

• 2018/19: 50% of interest deducted as normal and 50% at basic rate

• 2019/20: 25% of interest deducted as normal and 75% at basic rate

• 2020/21 onwards: all interest relieved at basic rate only

So, how will it work in practice?

As it is usually easier to follow an example we have provided below two worked examples for you to consider.

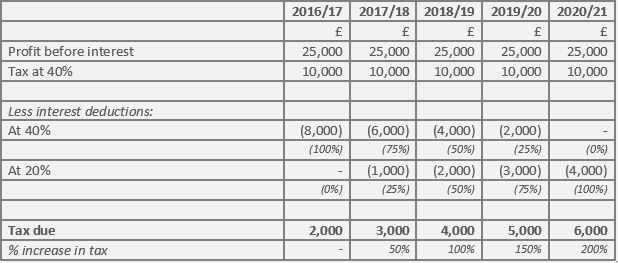

Example 1

Jennifer has a salary from her IT job in excess of the higher rate tax threshold and also receives annual rental income of £25,000 before deductions of mortgage interest of £20,000. Jennifer’s tax liabilities on her rental income will be as follows:

For Jennifer, the new restrictions will increase her tax by 200% and from 2020/21 her tax bill will actually be in excess of her profits.

However, the restrictions do not just affect the higher rate tax payers but are also likely to extend to many landlords who are currently basic rate tax payers or even to those who are making rental losses, as can be seen in Example 2:

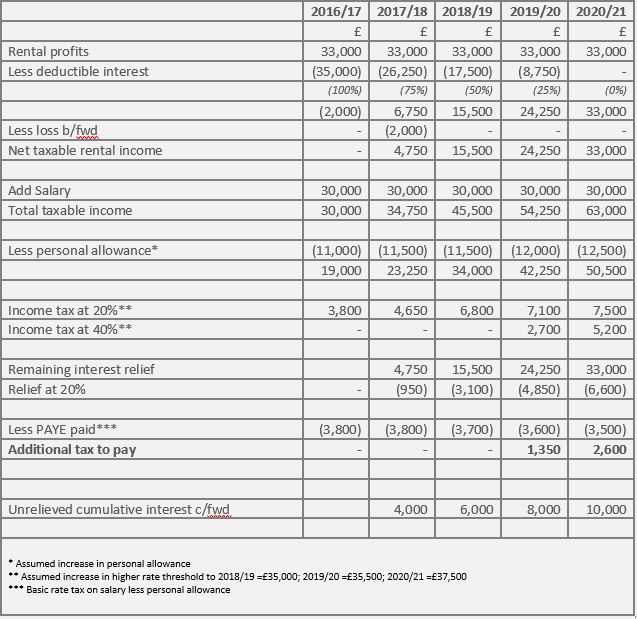

Example 2

Sam has a salary income from his teaching job of £30,000. He also has a portfolio of residential rental properties with annual income of £33,000 on which he pays annual mortgage interest of £35,000, making a net loss of £2,000 which he covers from his salary. The new changes will affect Sam as follows:

From the example above, we can see that although Sam continues to make net rental loss each year from 2019/20 tax year he will have additional tax liability to pay.

What can be done?

As with all tax matters there is never a one solution that fits all. Landlords would need to carefully consider their individual circumstances and seek professional tax advise where possible. However, some options to think about are:

- Consider whether the rental income route is still a viable option for you or should you be exiting?

- Increase rents so that the extra cost is passed to your tenant, however, this may not always be commercially viable as you could be priced out of the market.

- Focus on costs by getting lower mortgage rate, reducing mortgage size or considering buy-to-let off-set mortgages.

- Place your property in a company structure. You will then pay corporation tax which is lower and you will be able to deduct all of the mortgage interest. However, be mindful of potential stamp duty and capital gains tax implications as well profit extraction complications. This route may also narrow your mortgage options.

- Transfer ownership of one or more of your properties to a spouse provided he/she is a lower rate tax payer.

- Plan ahead and act now in order to avoid stress sale in future. Do not wait till 2020/21.

If you feel that issues highlighted in this article are likely to affect your business and would like to discuss this further with one of our specialist, you can contact AVEY of London on:

Tel: 01707 691 783

Email: info@aveyoflondon.co.uk

This guidance is designed to alert to an important issue of general application. It is not intended to be a definitive statement covering all aspects of the related legislation. It is only a brief summary and no action should be taken without consulting the detailed legislation or seeking professional advice.

No responsibility for any person acting or referring to act as a result of any material contained in this guidance can be accepted by AVEY of London.