IFRS 16 is a new leasing standard issued in January 2016, effective for periods beginning on or after 1 January 2019 (subject to EU endorsement).

The standard effectively eliminates operating lease accounting, with a few minor exceptions, requiring companies (lessees) to recognise all leases on the balance sheet.

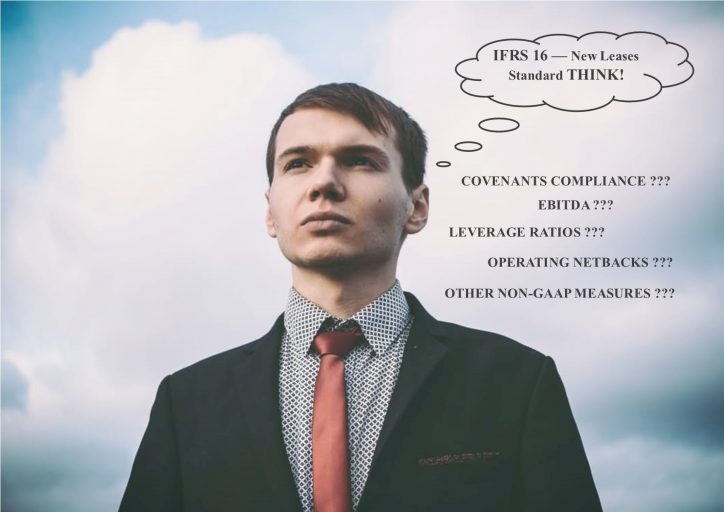

Accordingly, for companies with material off balance sheet leases covenants compliance is likely to be one of the key areas of concern, as well as various other financial metrics such as EBITDA, leverage ratio, operating netbacks, etc.

There is a wide range of various arrangements that typically exist within Mining and Oil & Gas industry which may fall within the scope of IFRS 16 and therefore affect future reporting, such as:

- services contracts including equipment used to deliver a service such as drilling rigs, compressors and tanks;

- shipping, freight and other transportation arrangements, including railway infrastructure and harbour loading services contracts;

- use of gas pipelines and processing facilities;

- refining, processing, tolling and storage arrangements.

There could also be other arrangements not specifically related to Mining or Oil & Gas activities such as rentals of vehicles, office space and furniture.

Although IFRS 16 doesn’t take effect until January 2019, to minimise the impact of the new standard it is highly advisable for companies to give the standard early attention.

The key requirements of the new leases standard and the practical considerations for companies within Mining and Oil & Gas industry are detailed further in our recent publication which can be accessed here.

At AVEY of London we have specialist knowledge of IFRS and can provide guidance on the changes that will affect your business as well as assist with application and interpretation of the new requirements.

Should you require further information or assistance you can contact AVEY of London on:

Tel: 01707 691 783

Email: info@aveyoflondon.co.uk

This guidance is designed to alert to an important issue of general application. It is not intended to be a definitive statement covering all aspects of the related legislation. It is only a brief summary and no action should be taken without consulting the detailed legislation or seeking professional advice. No responsibility for any person acting or referring to act as a result of any material contained in this guidance can be accepted by AVEY of London.